Key takeaways from seven of the biggest staffing firms in the UK

From sector growth to international expansion, we’ve summarised the annual reports from seven of the largest recruitment and staffing agencies that operate within the UK.

Summary

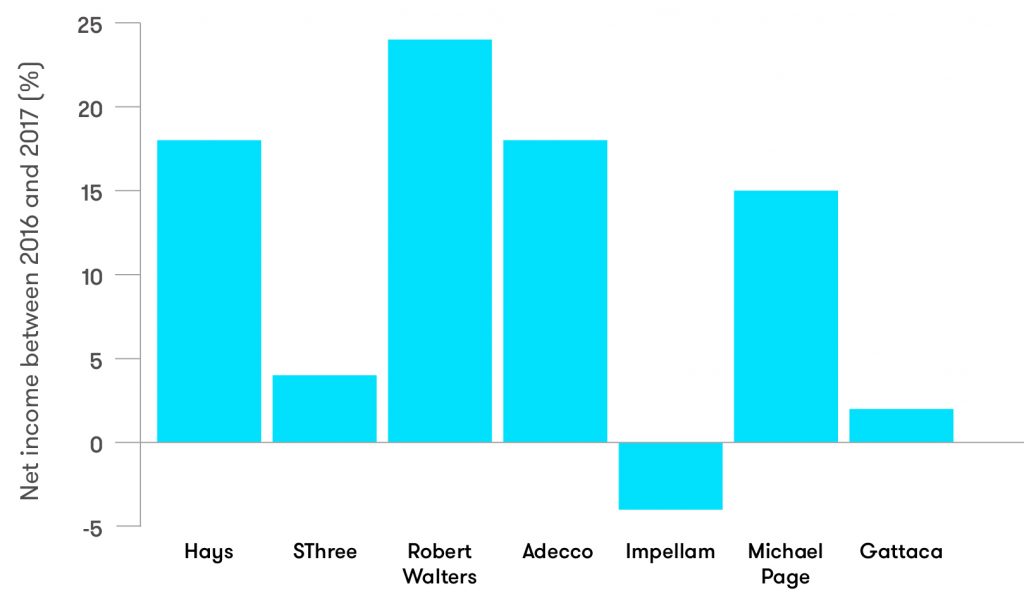

Hays’ net income increased 18% between 2016 and 2017. Split 59/41 between contract and perm, placement volume grew 8% overall with permanent growing 4% (70,000 placements) and contract doubling perm to reach 9% (240,000).

Overall, headcount grew 9% to 10,000 employees across Asia Pacific, Continental Europe & ROW, UK & Ireland, with UK & Ireland receiving the highest increase growing 70% from 2,024 to 3,458 employees.

UK

- Contract placements vs perm 56/44

- Most popular sectors: Accountancy & Finance, Construction & Property, Office Support, Education, IT & Banking

Continental Europe & Rest of World

- Contract placements vs perm 62/38

- Key Sectors: IT, Engineering, Accountancy & Finance, Construction & Property, Life Sciences and Sales & Marketing

Asia Pacific

- Contract placements vs perm 55/45

- Key Sectors: Construction & Property, Accountancy & Finance, IT, Office Support, Banking, Sales & Marketing

Predictions for 2018

- Drive further growth in their Temp/Contracting business in new/existing markets, including France, Japan, Canada and the US

- Biggest profit growth opportunity coming from Germany – “Germany, which represented 49% of the division’s net fees, delivered strong growth of 14% and a record net fee performance in the year. This was underpinned by strong growth across Contracting and Temp, which together grew by 13%, while perm net fees grew by an excellent 27%”

Summary

SThree’s gross profit increased 4% between 2016 and 2017. Split 71/29 between contract and perm, the number of contract placements grew 12% (9,078 / 10,197) although the number of runners since 2012 has increased by a staggering 99%.

Continental Europe and the USA combined now represent nearly 70% of their contract runners, up from 65% in 2016. Overall, headcount grew 11% to 2,866 employees, with 15% of that in contract and 3% in perm.

UK

- Brexit negotiations and the UK’s snap general election affected market confidence leading to a decline in both divisions: contract gross profit down 11% and perm down 22%, a total of 14% down.

Continental Europe

- Accounts for 52% of activity, up 3% from 2016

- Entered new countries in Austria and Spain and expanded there presence in France by opening new offices in Toulouse and Lyon.

- Contract growth YoY was across all sectors and driven by Continental Europe, which was up 17%.

- The Netherlands was a key highlight for the company: gross profit had an increase of 20%, their contract business grew by 27%, the number of contract runners up 21% although the perm side declined by 7%.

USA

- 22% of group activity comes from the USA, up 2% from 2016

- Contract placements vs perm 69/31

- The USA was SThree’s fastest-growing region in 2017, with gross profit up 18%

- Both contract and perm placements were up 21% and 12% respectively

- Contract growth YoY in the USA is up 21% across all sectors

Predictions for 2018

- SThree expect to continue to focus on geographies that meet criteria for investment, in particular, the USA, Germany and The Netherlands.

- SThree hopes to expand their employed contractor model to create new opportunities for their contract business in Continental Europe.

- Continue to open new offices in focus markets, e.g. Washington in the USA.

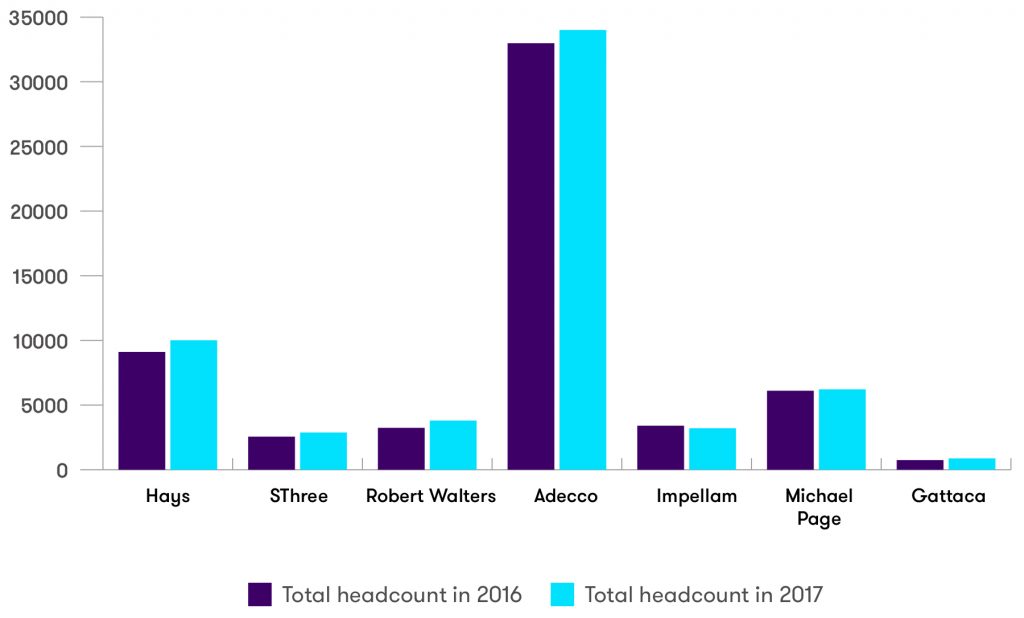

Net fee income chart

Chart comparing net fee income across all seven businesses

Summary

Robert Walter’s gross profit increased 24% between 2016 and 2017. Split 68/32 between contract and perm. They also saw an improvement in their debtor days, which decreased to 28 days from 29 days in 2016. Overall, headcount grew 17% from 3,229 to 3,793.

UK

- Accounts for 29% of net fee income

- Revenue was £569.6m (2016: £480.6m), net fee income increased by 16% to £100.9m (2016: £86.7m) and operating profit increased by 84% to £11.8m (2016: £6.4m)

- Key Sectors: growth was strongest across technology, legal, financial services and commerce finance.

Continental Europe

- Accounts for 23% of net fee income

- Revenue was £189.1m (2016: £147.0m), net fee income increased by 34% to £80.6m (2016: £60.1m) and operating profit increased by 168% to £11.3m (2016: £4.2m).

- Belgium, Germany, Portugal, The Netherlands and Spain all delivered net fee incomes increases of 20%+.

Asia Pacific

- Accounts for 40% of net fee income

- Revenue was £370.2m (2016: £348.6m), net fee income increased by 16% to £136.6m (2016: £117.6m) and operating profit increased by 21% to £17.7m (2016: £14.7m).

- Japan enjoyed another record year in Tokyo and Osaka.

Rest of the Word

- Revenue was £36.9m (2016:£22.3m), net fee income increased by 93% to £27.1m (£26.2m) (2016: £14.0m) and operating profit increased by 16% to £1.1m (2016: £0.9m)

- Market conditions in Brazil remain challenging but it has been positive to see our business deliver in excess of 50% growth in net fee income year-on-year.

- The new business in Canada has started well whilst in the US, although financial services remains tough, other market sectors, particularly technology and digital, continue to be strong.

Predictions for 2018

Canada Growth opportunity – Canada represents a strong, long-term growth opportunity for the Group. In this heavily commission driven market their non-commission and quality driven approach is a key differentiator.

Employee headcount chart

Chart comparing employee headcount growth across all seven businesses

Summary

Adecco’s gross margin was 18%. 110,000 perm placements were made during 2017. Along with that, they had revenue growth of 6%, down to strong performance in most European markets. Overall, headcount grew 3% to 34,000 employees worldwide.

UK & Ireland

In the UK & Ireland representing 26% of the segment, revenue development was strong with growth of 14% at constant currency driven by new large client wins. Although impacted by lower client and candidate confidence due to economic and political uncertainty related to the process of exiting the European Union.

Europe

- Revenues in France increased by 8% to €5,350m, temporary staffing revenues in France grew by 8% while permanent placement revenues grew by 14%.

- In Germany, Austria and Switzerland revenues were €2,185m, up 1% in constant currency and flat on a reported basis.

- Revenues in Benelux & Nordics increased by 10% to €2,079m. Currency fluctuations had no impact on the revenues while acquisitions had a positive impact of 1%. Organically, revenues increased by 9%. In Belgium, The Netherlands and Luxembourg revenues increased by 10%.

- In the Nordics revenues were up 7% organically with double-digit growth in Norway and Sweden while Denmark declined due to the completion of a few large client projects.

- Italy revenues had an increase of 25%, to €1,837m, including 30% growth in permanent placement. Growth was strong across all major sectors, including manufacturing, automotive, chemicals and logistics.

Rest of the World

In Japan, revenues in 2017 were €1,276m, Revenues grew by 7% in temporary staffing and by 27% in permanent

Predictions for 2018

- Digitisation, big data and advances in artificial intelligence are also transforming the staffing and recruitment industry itself and will continue to do so.

- Future growth in Professional Staffing & Solutions will be supported by opportunities arising from megatrends such as skills imbalances and the new demographic mix.

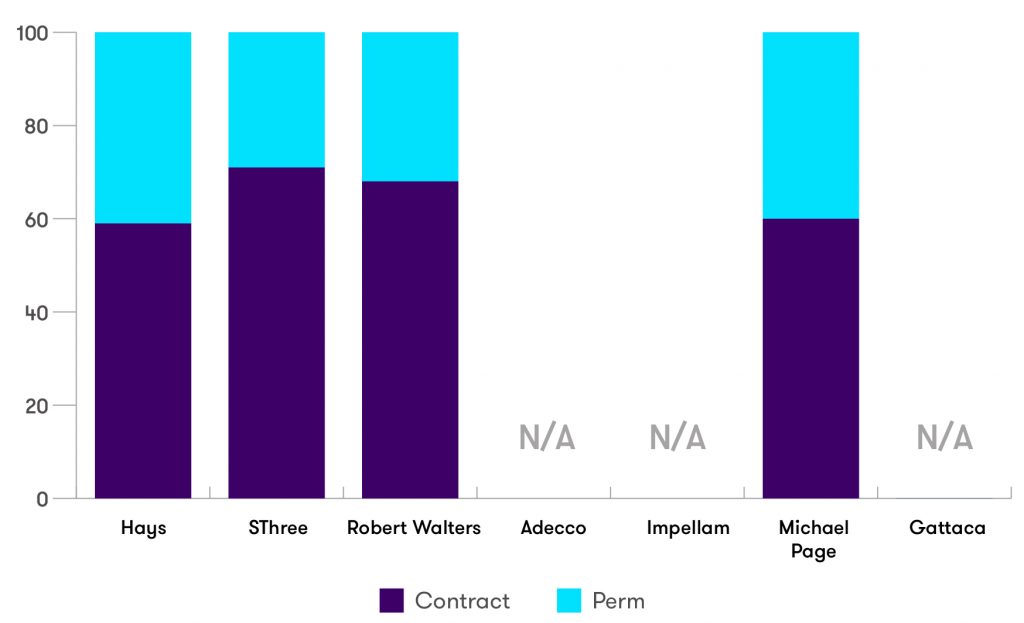

Contract/Perm spilt chart

Chart comparing the contract vs perm spilt across all seven businesses – N/A has been used for when there isn’t any contract/perm reported

Summary

Impellam’s gross profit in the UK and EMEA decreased 4% between 2016 and 2017, however they saw an increase of 3% on the US side of their business. Headcount also decreased from 3,400 to 3,200, a decrease of 6%.

UK

The UK education market is also challenging. Continued austerity measures, coupled with the rapid acceleration of teachers leaving the profession, have created a perfect storm of supply and demand dissonance.

Impellam continue to believe in the attractiveness of this market for the long term but recognise the need to rebalance the needs of government, schools, teachers and providers.

International

In mainland Europe, America and Australia, economic factors are more encouraging. Jobs are being created, and employment is rising. Changes in the world of work are leading to shifting employment patterns, and employers are increasingly open to working with staffing providers who are experienced in managing contingent employment models.

Demand for science, engineering, technology and healthcare skills is growing in these markets.

Gig Economy

- Contingent and contracting work – the ‘gig economy’ – now accounts for up to a third of the global workforce.

- Economic and societal shifts, technological advancement, talent shortages and new business models mean that people’s expectation of work and the way they choose to work are evolving.

- As permanent workforces contract over the coming years, reliance on flexible workers will increase, so employers will have to work hard to attract and retain these people.

Predictions for 2018

- Technology will grow as a sector and transform the roles required in others.

- Roles requiring intuition and relationship building will grow, including skill-short areas such as healthcare and education, alongside hospitality and the creative industries.

- Uncertainty around Brexit will continue to have an impact; although employment is growing and part-time and temporary work is increasing. Public sectors such as medical, care and teaching continue to be affected by government austerity and a globally mobile workforce who seek better opportunities elsewhere in the world.

Michael Page’s 15% increase in revenue was mirrored by 15% increase in gross profit between 2016 and 2017. Split 60/40 between contract and perm, the value of contract/temp work accounted for 25% of the overall group performance, an increase of 16% compared to the previous year. Overall, the group saw their headcount grow 2% from 6,099 to 6,214 employees.

UK

- Contract placements vs perm 30/70

- Most popular sectors: Engineering (+6%), Property & Construction (+10%) and Technology (+7%), performed well. However, market conditions in our Legal discipline (-11%) and Sales and Marketing disciplines were more challenging, with Marketing down 11%.

Europe

- European markets performed very well throughout 2017, with many having record-breaking years, there were increases of 25% in France, 12% in Germany and 16% in Spain.

USA

- In North America, our gross profit increased by 18% in constant currencies. This was driven by the US (+ 21%) where there was strong performances from our regional offices including Boston, Chicago and Los Angeles.

Asia Pacific

- Greater China returned to growth in the year up 14%

- South East Asia was up 12% on the prior year driven by growth in Indonesia and Malaysia, up 48% and 11% respectively.

- Despite challenging market conditions, Singapore returned to growth in the second half of the year.

- Japan, saw growth of 23% and delivered a record year

Predictions for 2018

Invest through cycles in large, high potential markets of Germany, Greater China, Latin America, South East Asia and the US to achieve scale and a market leading position.

Summary

Gattaca’s net income increased 2% between 2016 and 2017. There were 4,000 perm placements made throughout 2017, and finally, the headcount has grown 17% from 740 to 870 employees.

UK

Ongoing Brexit negotiations, IR35 tax changes and the 2017 general election have caused economic and political uncertainty and affected confidence in the job-hiring market. Demand for new hires, along with candidate availability, has been flat.

International

- Established a presence in Germany due to the growing engineering market in Bavaria.

- There was a 96% growth YOY in the USA, in engineering.

Sector Highlights

- The aerospace division grew by 13%

- Contract engineering grew by 4%, perm was down 26%

- Demand for manufacturing skills on a temporary basis was consistently high, particularly within the FMCG, consumer electronics and defence sectors.

- The converging engineering technology market, where we supply software, electronics and automation specialists across our engineering sectors, was the stand-out performer, with 19% year-on-year NFI growth.

Gig Economy

The lines between contract and permanent workforces are blurring as candidates look for the right project to suit their short to medium term plans. We have seen a growth in ‘statement of work’ roles – those taken on for specific activities, deliverables or time frames.

Predictions for 2018

- Increased demand for skills in areas such as data science and data analytics.

- “We are now well placed strategically to take advantage of the increasing convergence between the engineering, IT and telecoms skill sets, and to grasp the opportunities presented by infrastructure investment commitments around the world, particularly those made by the UK and US Governments”.